2026 Medicare Part D Changes: Save $300 Annually on Prescriptions

Understanding the 2026 Medicare Part D Changes: How to Save an Average of $300 Annually on Prescriptions

Navigating the complexities of Medicare can often feel like deciphering a secret code, especially when it comes to prescription drug coverage. However, significant changes are on the horizon for Medicare Part D 2026 that promise to bring much-needed relief to millions of beneficiaries. These updates, primarily driven by the Inflation Reduction Act of 2022, are designed to make prescription medications more affordable and predictable. For many, this could translate into an average annual saving of $300 or more on out-of-pocket drug costs. Understanding these changes now is crucial for planning and maximizing your benefits.

The Evolution of Medicare Part D: A Brief History and the Need for Change

Before diving into the specifics of Medicare Part D 2026, it’s helpful to understand the program’s origins and why these changes are so vital. Medicare Part D was established in 2003 through the Medicare Modernization Act, coming into effect in 2006. Its primary goal was to help Medicare beneficiaries cover the costs of prescription drugs, a critical gap in traditional Medicare Parts A and B.

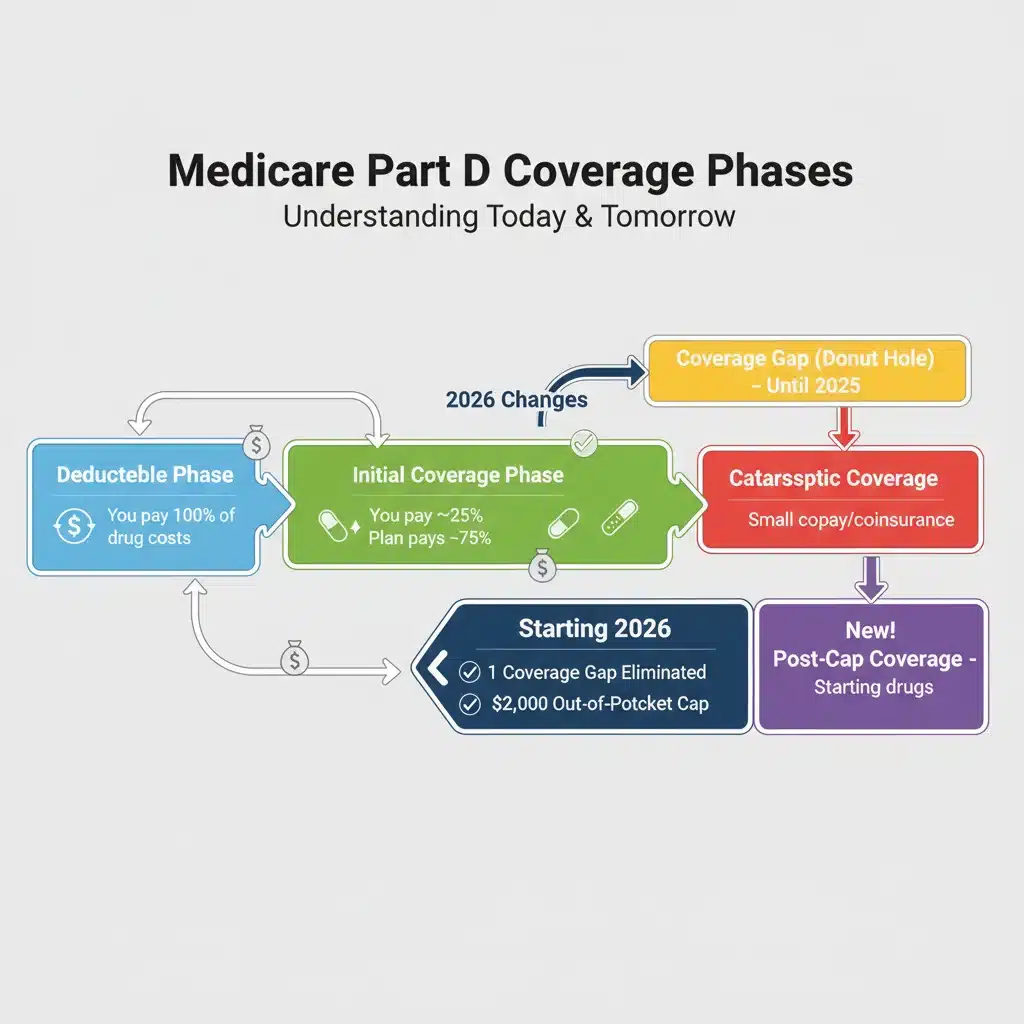

However, over the years, the structure of Part D has faced criticism, particularly concerning its complex coverage phases, including the infamous ‘donut hole’ or coverage gap, and the lack of an out-of-pocket spending cap. While the Affordable Care Act (ACA) and subsequent legislation gradually closed the donut hole, beneficiaries could still face unlimited out-of-pocket costs once they reached the catastrophic coverage phase, which could be financially devastating for those with high-cost medications.

The rising cost of prescription drugs in the United States has been a persistent concern, impacting seniors and individuals with chronic conditions disproportionately. This financial burden often led to difficult choices between essential medications and other necessities, or even non-adherence to prescribed treatments, leading to poorer health outcomes. The legislative efforts culminating in the Inflation Reduction Act (IRA) were a direct response to these challenges, aiming to inject greater affordability and equity into the prescription drug landscape. The changes to Medicare Part D 2026 are a pivotal part of this broader reform.

Key Changes to Medicare Part D in 2026: What You Need to Know

The Inflation Reduction Act introduces several groundbreaking reforms to Medicare Part D 2026 that will significantly alter how beneficiaries pay for their medications. These changes are designed to provide greater financial predictability and reduce the burden of high drug costs. Let’s break down the most impactful provisions:

1. The Landmark $2,000 Out-of-Pocket Spending Cap

Perhaps the most transformative change coming in Medicare Part D 2026 is the implementation of a $2,000 annual out-of-pocket spending cap for prescription drugs. This is a game-changer for beneficiaries, especially those with chronic conditions requiring expensive medications. Currently, while there’s a coverage gap, there’s no true cap on how much a beneficiary might pay in a year once they reach the catastrophic phase. In this phase, beneficiaries are responsible for 5% of their drug costs, which, for very high-cost drugs, can still amount to thousands of dollars.

With the $2,000 cap, once your out-of-pocket spending on covered Part D drugs (including your deductible, copayments, and coinsurance) reaches this threshold, you will pay nothing for the remainder of the year. This provides immense financial security and peace of mind, ensuring that no matter how expensive your medications are, your annual costs will not exceed $2,000.

This cap is projected to save beneficiaries an average of $300 annually, but for those with very high drug costs, the savings could be substantially higher, potentially thousands of dollars per year. It effectively eliminates the 5% coinsurance in the catastrophic phase, shifting the financial responsibility to plans and drug manufacturers.

2. Elimination of the Catastrophic Coverage Phase Coinsurance

As a direct consequence of the $2,000 out-of-pocket cap, the 5% coinsurance requirement in the catastrophic coverage phase will be eliminated starting in Medicare Part D 2026. Previously, after reaching a certain spending threshold, beneficiaries entered the catastrophic phase where they paid 5% of their drug costs, with no upper limit. This system left many vulnerable to exorbitant costs for life-sustaining medications.

The removal of this coinsurance means that once you hit the $2,000 cap, your out-of-pocket costs for covered Part D drugs become zero for the rest of the year. This is a significant improvement, ensuring that once a beneficiary has paid their share up to the cap, they are fully protected from further drug expenses.

3. Expanded Eligibility for Low-Income Subsidies (LIS/Extra Help)

Another crucial enhancement under the Medicare Part D 2026 reforms is the expansion of eligibility for the Low-Income Subsidy (LIS) program, often referred to as ‘Extra Help.’ This program assists individuals with limited income and resources in paying for their Part D premiums, deductibles, copayments, and coinsurance.

Currently, partial LIS benefits are available to individuals with incomes between 135% and 150% of the federal poverty level (FPL). Starting in 2024 (a precursor to the 2026 changes), the IRA expanded full LIS benefits to those with incomes up to 150% of the FPL. This means more individuals will qualify for comprehensive financial assistance, significantly reducing their prescription drug costs and making them virtually immune to the complexities of the Part D benefit design. This expansion aims to reduce health disparities and ensure that financial constraints do not prevent access to necessary medications.

4. Manufacturer Discounts in the Catastrophic Phase

While not a direct change for beneficiaries in terms of what they pay, it’s important to understand the underlying mechanism that supports the new $2,000 cap. Under the IRA, drug manufacturers will be required to provide discounts on brand-name drugs in the catastrophic phase. This shift in financial responsibility from beneficiaries and the federal government to manufacturers is a key component of how the new cap is funded and sustainable. This provision encourages manufacturers to consider pricing more carefully, as they now bear a greater share of the cost for high-utilization, high-cost drugs.

How These Changes Translate to Savings: An Average of $300 Annually

The projected average annual savings of $300 for beneficiaries under Medicare Part D 2026 is a conservative estimate. The actual savings will vary significantly based on individual prescription drug needs and current spending habits. However, for many, this figure represents a tangible improvement in their financial well-being.

Consider a beneficiary who currently spends $2,500 out-of-pocket annually on prescription drugs. In 2026, their out-of-pocket costs would be capped at $2,000, resulting in an immediate saving of $500. For someone with even higher drug costs, say $5,000 annually, the savings would be $3,000. These are not insignificant amounts, especially for individuals living on fixed incomes.

The $300 average saving comes from a broader analysis of how these changes will impact the entire beneficiary population, factoring in those who currently spend less than the $2,000 cap, those who spend just over it, and those who spend significantly more. The key takeaway is that for anyone who currently faces high prescription drug costs, the 2026 changes offer a substantial financial safeguard.

Who Benefits Most from the 2026 Part D Reforms?

- Individuals with High-Cost Chronic Conditions: Those who rely on expensive specialty drugs for conditions like cancer, rheumatoid arthritis, multiple sclerosis, or certain autoimmune diseases will see the most significant financial relief due to the $2,000 cap.

- Low-Income Beneficiaries: The expanded eligibility for Extra Help will ensure that more individuals who struggle to afford their medications receive comprehensive financial assistance, virtually eliminating their out-of-pocket costs.

- Anyone Approaching the Catastrophic Phase: Even beneficiaries with moderately high drug costs who previously entered the catastrophic phase and paid 5% coinsurance will benefit from the elimination of this cost-sharing.

- All Beneficiaries: While the direct financial impact will vary, the overall predictability and reduction of catastrophic risk benefit all Part D enrollees, offering greater peace of mind.

Preparing for Medicare Part D 2026: Strategies for Maximizing Your Savings

While the changes in Medicare Part D 2026 are largely beneficial, proactive planning can further enhance your savings and ensure you make the most of the new system. Here are some strategies to consider:

1. Review Your Current Prescription Drug Usage and Costs

Take stock of all your current prescription medications, including dosage and frequency. Gather your Explanation of Benefits (EOB) statements from your current Part D plan to understand your annual out-of-pocket spending. This will give you a baseline to compare against the new $2,000 cap and estimate your potential savings. Knowing your typical drug expenses is the first step in strategic planning.

2. Understand the New Plan Structures

As 2026 approaches, Part D plans will adjust their offerings to align with the new regulations. Pay close attention to how plans structure their formularies (list of covered drugs), deductibles, and copayments/coinsurance, especially in the initial coverage phase. While the $2,000 cap provides ultimate protection, minimizing costs before reaching that cap is still beneficial. Some plans may offer $0 deductibles or lower copays for preferred generics, which can save you money throughout the year.

3. Re-evaluate Your Plan During Open Enrollment

Each year during the Annual Enrollment Period (AEP), from October 15th to December 7th, you have the opportunity to review and change your Medicare Part D plan. This will be an especially critical period in late 2025 as plans finalize their 2026 offerings. Use Medicare’s Plan Finder tool on Medicare.gov to compare plans based on your specific medications and estimated costs. The tool will be updated to reflect the Medicare Part D 2026 changes, allowing for accurate comparisons.

4. Check Your Eligibility for Extra Help (LIS)

If your income and resources are limited, re-evaluate your eligibility for the expanded Low-Income Subsidy (LIS) program. Even if you didn’t qualify in previous years, the expanded criteria for full LIS benefits, effective in 2024, might make you eligible for significant premium and cost-sharing assistance in 2026. You can apply for Extra Help through the Social Security Administration (SSA).

5. Explore Generic and Preferred Brand Alternatives

Even with the $2,000 cap, using generic or preferred brand-name drugs can help you reach the cap slower or save you money if your annual costs typically fall below the cap. Always discuss potential alternatives with your doctor and pharmacist to ensure they are medically appropriate for you.

6. Utilize Manufacturer Patient Assistance Programs (PAPs)

While the new Part D changes provide substantial relief, some drug manufacturers offer Patient Assistance Programs (PAPs) that can help cover out-of-pocket costs for specific brand-name medications. These programs are separate from Medicare, but can still be a valuable resource, especially for costs incurred before reaching the $2,000 cap. Check directly with drug manufacturers or through organizations that help connect patients with PAPs.

7. Understand Other Cost-Saving Measures

Beyond the structural changes, continue to employ common strategies for saving on prescriptions: ask your doctor for 90-day supplies for maintenance medications to potentially reduce dispensing fees, explore mail-order pharmacy options which often offer lower costs, and always compare prices at different pharmacies. While the $2,000 cap is a safeguard, being a savvy consumer still pays off.

The Broader Impact of the Inflation Reduction Act on Prescription Drug Costs

The changes to Medicare Part D 2026 are part of a larger legislative effort to control prescription drug costs through the Inflation Reduction Act. While the $2,000 cap and LIS expansion are key components for Part D beneficiaries, other provisions of the IRA also play a role in the broader drug pricing landscape:

- Drug Price Negotiation: Starting with a limited number of drugs in 2026, Medicare will gain the power to negotiate prices for certain high-cost prescription drugs directly with pharmaceutical manufacturers. This marks a historic shift and is expected to drive down costs for some of the most expensive medications.

- Inflation Rebates: The IRA requires drug companies to pay rebates to Medicare if they raise the prices of certain drugs faster than the rate of inflation. This provision aims to curb unjustified price increases and keep drug costs more stable over time.

- Insulin Cap: As of 2023, the cost of insulin for Medicare beneficiaries is capped at $35 per month per covered prescription, regardless of their plan’s deductible or coverage phase. This was a direct, immediate relief for millions of diabetics.

- Vaccines: Starting in 2023, Medicare Part D plans began covering recommended adult vaccines (such as shingles and RSV vaccines) with no cost-sharing. This removes a significant barrier to preventative care.

These broader changes collectively contribute to a more affordable and equitable healthcare system, with the Medicare Part D 2026 reforms being a cornerstone for direct beneficiary savings on out-of-pocket drug costs.

Potential Challenges and Considerations

While the Medicare Part D 2026 changes are overwhelmingly positive, it’s also important to be aware of potential challenges or considerations:

- Initial Coverage Phase Costs: While the $2,000 cap protects against catastrophic costs, beneficiaries will still be responsible for deductibles and copayments in the initial coverage phase. Strategically choosing a plan that minimizes these upfront costs can still be beneficial.

- Formulary Changes: Part D plans can change their formularies annually. It’s crucial to ensure your specific medications are covered by your chosen plan each year, especially during open enrollment.

- Impact on Premiums: While the IRA aims to reduce out-of-pocket costs, there’s always a possibility that plan premiums could see some adjustments as plans adapt to the new benefit structure and manufacturer discounts. However, the overall goal is to reduce the total burden on beneficiaries.

- Non-Covered Drugs: The $2,000 cap applies only to covered Part D drugs. If you take medications not on your plan’s formulary or those specifically excluded from Part D coverage (e.g., over-the-counter drugs, weight loss drugs), these costs will not count towards the cap.

Staying informed and actively reviewing your options will be key to navigating these aspects effectively.

Conclusion: A New Era of Affordability for Medicare Part D 2026

The year 2026 marks a pivotal moment for Medicare Part D beneficiaries. The implementation of a $2,000 out-of-pocket spending cap, the elimination of catastrophic phase coinsurance, and expanded eligibility for low-income subsidies are monumental steps towards making prescription drugs more affordable and predictable. These changes, driven by the Inflation Reduction Act, are expected to save beneficiaries an average of $300 annually, with much higher savings for those with significant medication needs.

By understanding these reforms, reviewing your current prescription costs, and proactively planning during open enrollment, you can maximize your benefits and significantly reduce your financial burden. The future of Medicare Part D 2026 is one of greater financial security and improved access to essential medications, ensuring that seniors and individuals with disabilities can prioritize their health without breaking the bank. Stay engaged, stay informed, and prepare to take advantage of these transformative changes.