Navigating 2026 Capital Gains Tax Changes: Optimize Investments

Understanding the New Capital Gains Tax Rules in 2026: How to Optimize Your Investment Portfolio

As we approach 2026, the financial world is buzzing with discussions about the impending changes to capital gains tax rules. These revisions are not just minor adjustments; they represent a significant shift that could profoundly impact how investors manage their portfolios, realize gains, and plan for their financial future. For both seasoned investors and those new to the market, understanding these changes is paramount to optimizing investment strategies and minimizing tax liabilities. This comprehensive guide aims to demystify the new regulations, provide actionable insights, and equip you with the knowledge to navigate the evolving tax landscape effectively.

The term ‘capital gains’ refers to the profit an investor realizes when they sell a capital asset for a price higher than their purchase price. Capital assets can include stocks, bonds, real estate, and even collectibles. These gains are typically subject to taxation, with rates varying based on the holding period of the asset (short-term or long-term) and the investor’s income bracket. The upcoming changes in 2026 are expected to fine-tune these parameters, potentially altering the tax burden for many.

What are Capital Gains and Why Do They Matter for 2026?

Before delving into the specifics of the 2026 changes, it’s crucial to grasp the fundamentals of capital gains. A capital gain occurs when you sell an asset, such as a stock, bond, or real estate, for more than you paid for it. Conversely, a capital loss occurs when you sell an asset for less than its purchase price. These losses can often be used to offset capital gains and, in some cases, a limited amount of ordinary income.

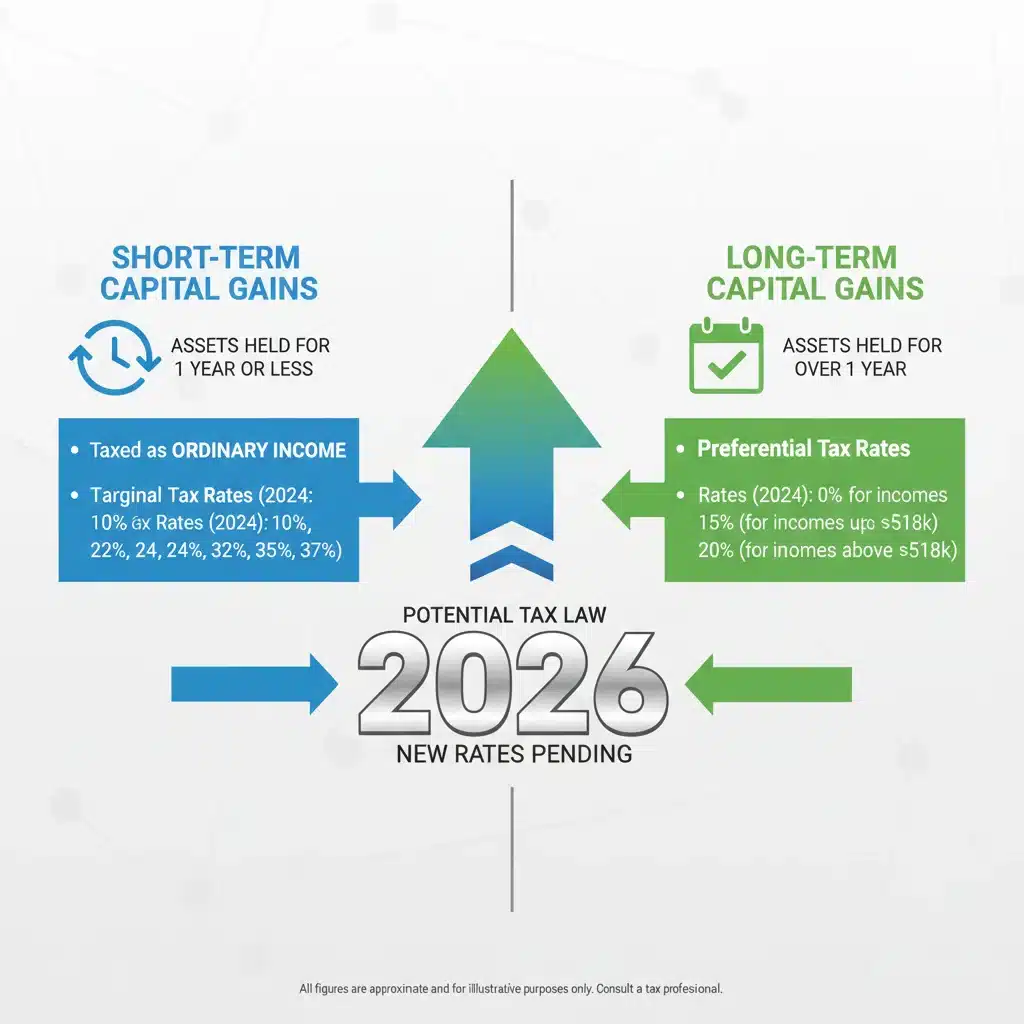

There are two primary categories of capital gains: short-term and long-term. Short-term capital gains are profits from assets held for one year or less. These are typically taxed at your ordinary income tax rates, which can be significantly higher than long-term rates. Long-term capital gains, on the other hand, are profits from assets held for more than one year. These often benefit from preferential tax rates, which are generally lower than ordinary income tax rates. The distinction between short-term and long-term is a critical aspect of capital gains tax planning, and it’s an area that could see significant adjustments with the capital gains 2026 rules.

Why do these changes matter? For investors, the tax implications of capital gains can significantly impact net returns. A higher tax rate means a smaller portion of your investment profits remains in your pocket. Therefore, understanding and adapting to new tax rules is not just about compliance; it’s about maximizing your wealth accumulation and ensuring your investment strategies remain efficient and profitable. The capital gains 2026 amendments are designed to potentially address various economic and social objectives, which could include revenue generation, wealth redistribution, or incentivizing certain types of investments. Regardless of the underlying motivations, the practical effect on investors will be tangible.

Key Anticipated Changes to Capital Gains Tax in 2026

While the final details are still subject to legislative processes, several key areas are widely anticipated to be affected by the capital gains 2026 reforms. These include potential adjustments to tax rates, alterations to the holding period definitions, and modifications to exemptions or deductions.

Potential Adjustments to Capital Gains Tax Rates

One of the most significant changes could be in the actual tax rates applied to capital gains. There’s speculation about potential increases in long-term capital gains rates, particularly for high-income earners. Historically, long-term capital gains rates have been kept lower to encourage long-term investment and capital formation. However, economic shifts and fiscal policy objectives can lead to reassessments of these rates. For instance, a move to align long-term capital gains rates more closely with ordinary income tax rates for certain income brackets has been a recurring discussion point. Such a change would necessitate a re-evaluation of investment horizons and asset allocation strategies for many investors. Understanding how these rate changes might apply to different income tiers is crucial for effective tax planning.

Revisions to Holding Period Definitions

Another area ripe for change is the definition of short-term versus long-term capital gains. The current one-year threshold has been a long-standing benchmark. However, there’s a possibility that this holding period could be extended. For example, if the definition of a long-term asset were to increase to two or three years, it would significantly impact trading strategies, particularly for those who frequently rebalance their portfolios or engage in shorter-term investments. This would force investors to consider holding assets for longer durations to qualify for potentially lower long-term rates, thereby influencing liquidity and investment decisions. The specific implications of such a change for the capital gains 2026 framework cannot be overstated.

Modifications to Exemptions and Deductions

Existing exemptions and deductions related to capital gains might also be subject to review. For example, the exclusion for capital gains on the sale of a primary residence, or certain favorable treatments for qualified small business stock (QSBS), could see adjustments. While these provisions are often designed to support specific economic activities or provide relief to homeowners, they are not immune to legislative changes. Any modifications in these areas could have substantial implications for real estate investors, entrepreneurs, and individuals planning to sell their homes. It’s essential to monitor these potential changes closely as they could significantly alter the net proceeds from such transactions under the capital gains 2026 rules.

Impact on Different Investment Types

The upcoming capital gains 2026 rules will not affect all investment types equally. Different assets have distinct characteristics and are often subject to varying tax treatments. Understanding these nuances is key to optimizing your portfolio.

Stocks and Bonds

For traditional equity and fixed-income investments, the primary impact will likely be on the distinction between short-term and long-term gains. If the holding period for long-term gains is extended, investors might need to adjust their trading frequency. For example, day traders or swing traders who realize short-term gains frequently could face a higher tax burden if ordinary income tax rates increase or if the definition of ‘short-term’ becomes broader. Conversely, buy-and-hold investors who maintain positions for several years might be less affected, assuming long-term rates remain preferential. The tax efficiency of dividend-paying stocks and municipal bonds, which offer tax-exempt interest, could also become more attractive in a higher capital gains tax environment.

Real Estate

Real estate investments, including rental properties and REITs (Real Estate Investment Trusts), have unique tax considerations. The sale of investment properties is subject to capital gains tax, and depreciation recapture can add another layer of complexity. If the capital gains 2026 rules increase rates, selling an investment property could result in a larger tax bill. Furthermore, any changes to the primary residence exclusion or 1031 exchange rules (which allow investors to defer capital gains taxes on the sale of investment property by reinvesting the proceeds into a similar property) would significantly impact real estate investors. It’s crucial for real estate investors to consult with tax professionals to understand the specific implications for their holdings.

Cryptocurrencies and Digital Assets

The taxation of cryptocurrencies and other digital assets has been a rapidly evolving area. Currently, the IRS generally treats cryptocurrencies as property for tax purposes, meaning they are subject to capital gains tax when sold, exchanged, or used to purchase goods or services. With the growing mainstream adoption of digital assets, it’s highly probable that the capital gains 2026 legislation will include more explicit guidelines and potentially new tax treatments for these assets. This could involve clearer definitions of holding periods, specific reporting requirements, or even different tax rate structures. Investors in this nascent asset class must stay informed about these potential developments to ensure compliance and optimize their digital asset portfolios.

Alternative Investments

Alternative investments, such as private equity, venture capital, hedge funds, and collectibles (art, antiques, precious metals), often have distinct tax treatments. These investments can involve complex structures and longer holding periods. The capital gains 2026 changes could influence the attractiveness of these assets, especially if long-term rates increase or if there are changes to carried interest taxation for fund managers. For collectibles, which are often taxed at higher capital gains rates (up to 28%), any increases in general capital gains rates could further amplify their tax burden. Diversification into alternative assets often requires a sophisticated understanding of their tax implications, which will become even more critical with the new rules.

Strategies to Optimize Your Investment Portfolio for 2026

Proactive planning is essential to mitigate the impact of the capital gains 2026 changes and optimize your investment portfolio. Here are several strategies to consider:

Harvesting Capital Losses

Capital loss harvesting is a time-tested strategy that becomes even more valuable in anticipation of higher capital gains taxes. This involves selling investments at a loss to offset realized capital gains. If your capital losses exceed your capital gains, you can typically deduct up to $3,000 of the remaining loss against your ordinary income, and carry forward any excess losses to future tax years. By strategically realizing losses before 2026, you can create a pool of losses to offset future gains that might be taxed at higher rates. This strategy requires careful timing and an understanding of the wash-sale rule, which prevents you from claiming a loss on a security if you buy a substantially identical security within 30 days before or after the sale.

Reviewing Asset Location and Allocation

Asset location refers to deciding where to hold different types of investments (e.g., in taxable accounts, IRAs, 401(k)s). Tax-inefficient assets, such as high-turnover funds or bonds generating taxable interest, might be better placed in tax-advantaged accounts where gains and income can grow tax-deferred or tax-free. Conversely, tax-efficient assets like individual stocks with low turnover or exchange-traded funds (ETFs) might be suitable for taxable accounts. As for asset allocation, re-evaluating your mix of stocks, bonds, and other assets in light of potential rate changes can help. If long-term capital gains rates increase significantly, you might consider adjusting your allocation towards assets that generate qualified dividends or tax-exempt income, or those with a lower likelihood of frequent taxable events.

Utilizing Tax-Advantaged Accounts

Maximizing contributions to tax-advantaged accounts like 401(k)s, IRAs (Traditional and Roth), HSAs (Health Savings Accounts), and 529 plans is always a sound strategy, and it becomes even more critical with impending tax changes. These accounts offer various tax benefits, such as tax-deferred growth (Traditional IRA, 401(k)), tax-free growth and withdrawals (Roth IRA, HSA if used for qualified medical expenses), or tax-free growth for educational expenses (529 plans). By sheltering your investments in these accounts, you can shield them from the immediate impact of higher capital gains 2026 taxes and potentially reduce your overall tax burden in retirement or for specific qualified expenses.

Considering Qualified Opportunity Zones (QOZs)

Qualified Opportunity Zones (QOZs) offer tax incentives for investments in designated economically distressed communities. Investors can defer or even eliminate capital gains taxes by investing realized capital gains into a Qualified Opportunity Fund (QOF). While this strategy has specific requirements and risks, it could become more attractive if capital gains 2026 rates increase significantly. The longer you hold your QOZ investment, the greater the tax benefits. This strategy is complex and requires thorough due diligence, but it can be a powerful tool for certain investors.

Donating Appreciated Assets to Charity

If you are charitably inclined, donating appreciated assets directly to a qualified charity can be a highly tax-efficient strategy. When you donate stock or other property held for more than a year, you generally don’t have to pay capital gains tax on the appreciation. Instead, you can typically deduct the fair market value of the assets as a charitable contribution, subject to certain limitations. This allows you to support causes you care about while avoiding capital gains taxes that might be higher under the capital gains 2026 rules.

Engaging in Tax-Loss Harvesting for 2025

As 2026 approaches, consider strategically harvesting capital losses in late 2025. This allows you to offset any gains realized in 2025 and potentially carry forward losses to offset gains in 2026 and beyond, when tax rates might be higher. This preemptive move can significantly reduce your future tax liability. Consult with a financial advisor to devise a personalized tax-loss harvesting plan that aligns with your investment goals and risk tolerance.

The Importance of Professional Guidance

Navigating the complexities of tax law, especially with impending changes like the capital gains 2026 reforms, requires specialized expertise. While this guide provides a general overview and actionable strategies, every investor’s situation is unique. Factors such as your income level, investment portfolio composition, financial goals, and risk tolerance all play a crucial role in determining the most effective tax optimization strategies.

Financial Advisors

A qualified financial advisor can help you assess your current investment portfolio, understand the potential impact of the capital gains 2026 changes on your specific situation, and develop a tailored strategy. They can assist with asset allocation, asset location, and identifying opportunities for tax-loss harvesting or other tax-efficient investment vehicles. A good financial advisor will also stay updated on legislative developments and adjust your plan accordingly.

Tax Professionals (CPAs, Tax Attorneys)

For more intricate tax planning and ensuring compliance, consulting with a Certified Public Accountant (CPA) or a tax attorney is highly recommended. These professionals can provide expert advice on complex tax situations, help you interpret the specific language of the new tax laws, and ensure that your strategies are legally sound and optimized for your tax bracket. They can also assist with preparing your tax returns and addressing any questions or concerns that may arise regarding the capital gains 2026 rules.

Staying Informed and Adapting

The legislative process can be dynamic, and the final details of the capital gains 2026 changes may evolve as they move through Congress. It is crucial for investors to stay informed about these developments. Regularly checking reputable financial news sources, government publications (such as IRS announcements), and updates from your financial and tax advisors will help you remain ahead of the curve. Flexibility and adaptability will be key. Your investment strategy should not be static; it should be a living plan that can be adjusted in response to market conditions, personal circumstances, and changes in tax law.

The goal is not just to minimize taxes but to do so within the broader context of your financial objectives. Tax planning should always be integrated with your overall investment strategy, aiming to maximize after-tax returns while staying aligned with your risk tolerance and long-term goals. The changes coming in 2026 present both challenges and opportunities. By understanding the potential impacts and implementing strategic planning, you can position your portfolio for continued success.

Conclusion: Preparing for the Future of Capital Gains Tax

The anticipated changes to capital gains 2026 rules represent a significant moment for investors. While the exact contours of the new legislation are still being finalized, the general direction points towards a need for greater awareness and proactive planning. By understanding the fundamentals of capital gains, anticipating potential adjustments to rates and holding periods, and exploring various optimization strategies, investors can effectively navigate this evolving tax landscape.

Whether it’s through strategic tax-loss harvesting, optimizing asset location, maximizing tax-advantaged accounts, or exploring specialized investment vehicles like Qualified Opportunity Zones, there are numerous avenues to consider. Most importantly, engaging with qualified financial and tax professionals will provide invaluable guidance tailored to your unique financial situation. The future of capital gains taxation requires a thoughtful and informed approach. By taking steps now, you can ensure your investment portfolio is not only resilient to the changes but also positioned for optimal growth and tax efficiency in 2026 and beyond.